Adjustable-rate mortgages are usually most popular when borrowing costs are rising, yet Cotality data shows the opposite dynamic emerging in 2025 and early 2026. Even as average mortgage rates eased from about 7% to below 6.5% in early 2025, the share of ARMs climbed to nearly 21% of all mortgages, the highest level in roughly three years. That momentum continued into 2026, highlighting a structural affordability problem rather than a simple rate-cycle story.

Why the 30-Year Fixed Is Losing Its Affordability Edge

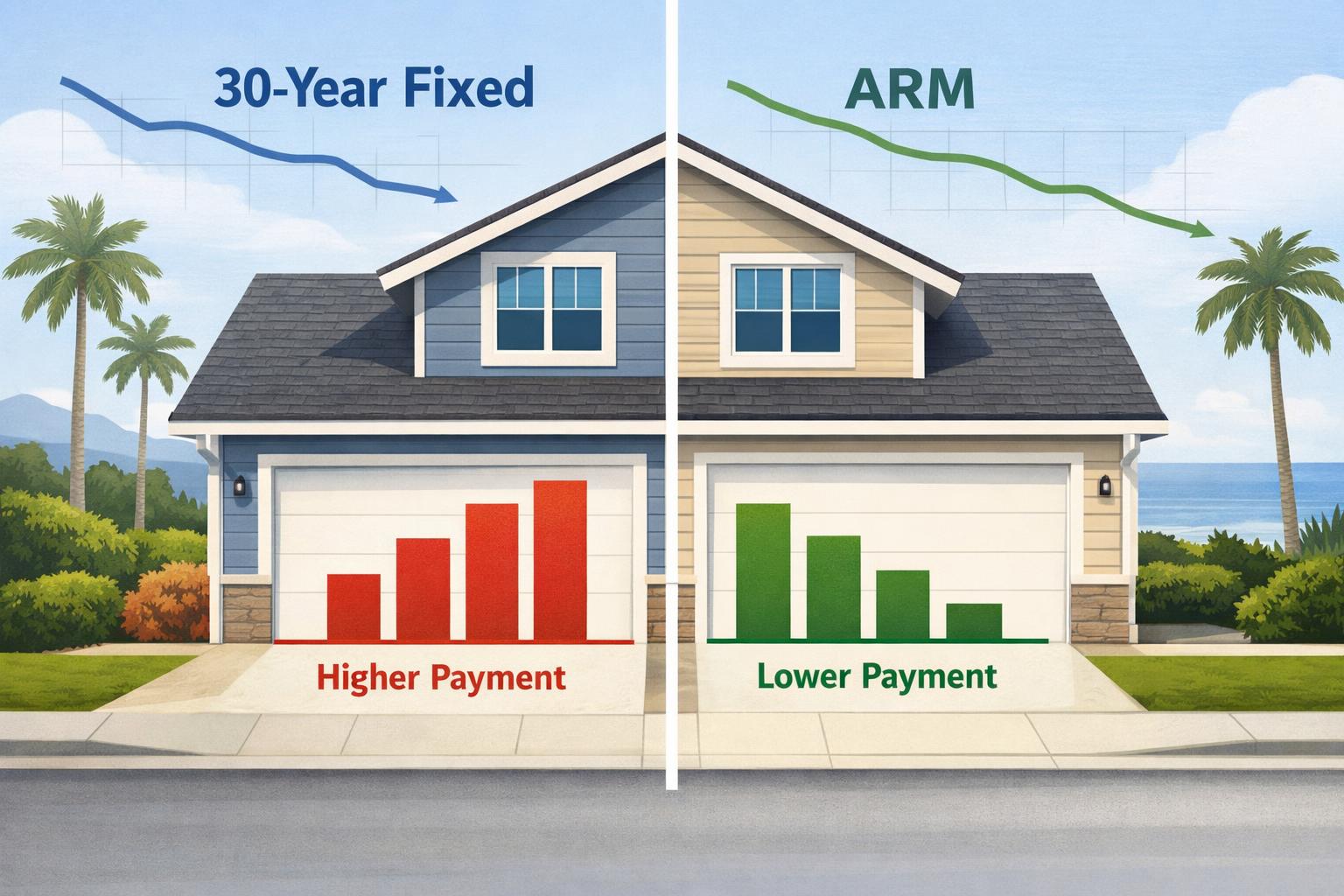

The 30-year fixed-rate mortgage has long been treated as the cornerstone of U.S. homeownership, offering decades of predictable payments and a hedge against inflation. But in today’s pricing environment, that stability can come at a steep upfront cost. With 30-year fixed rates around 6.1% in early 2026, many buyers find that the payment level tied to a fixed loan pushes a purchase out of reach, especially in high-cost metros.

Cotality’s analysis suggests that the loan type once considered the default tool for making ownership possible is, for some households, becoming a roadblock to qualifying at all. Instead of optimizing for lifetime stability, buyers are increasingly choosing financing that improves monthly cash flow in the first five to seven years.

The Fixed–ARM Rate Gap Is Driving Behavior

The spread between fixed and adjustable rates is at the heart of this shift. While a typical 30-year fixed rate sits near 6.1%, a 5/1 ARM is closer to 5.3%. On a $1 million loan in an expensive market, that 0.8 percentage point discount translates into almost $500 in monthly payment savings. For many borrowers, that difference is not just appealing — it is what allows them to qualify for the mortgage under today’s income and debt-to-income constraints.

Borrowers opting for these structures are effectively treating their mortgage rate as temporary. Many expect to refinance into a lower fixed rate later or to sell before the first reset hits. The trade-off is clear: accept future rate uncertainty in exchange for immediate payment relief.

High-Cost Markets Are Ground Zero for ARM Growth

The resurgence of ARMs is most striking in markets where home prices have remained elevated despite modest rate declines. In California, ARMs accounted for more than 31% of mortgage originations in 2025, according to Cotality’s public-records analysis. The District of Columbia saw ARM share around 28%, and Massachusetts hovered near 24%, underscoring how buyers in expensive coastal hubs are leaning on adjustable products to bridge the affordability gap.

Rather than a niche option for risk-tolerant borrowers, ARMs in these locations have become a mainstream tool for first-time buyers stretching into homeownership and for move-up buyers targeting pricier properties. Local price dynamics have not softened enough to make fixed loans comfortably affordable, so adjustable rates are doing more of the heavy lifting.

Loan Size Matters: ARMs Dominate in the Upper Tiers

The move toward ARMs is not limited to geography; it is also concentrated by price point. Cotality’s breakdown by loan size shows that adjustable products are gaining share in the middle and upper segments of the market, particularly for homes priced between about $400,000 and $1 million. By late 2025, ARMs represented roughly 15% of financing in this band.

At the very top of the market, ARMs are now the dominant structure. By December 2025, nearly half of mortgage originations above $1 million were adjustable-rate loans. Jumbo borrowers have more incentive to chase small shifts in rates because each fraction of a percentage point translates into substantial monthly and lifetime savings.

Modern ARMs: More Protections, Different Risks

Today’s ARMs are typically structured as 5/1 or 7/1 products, with an initial fixed period followed by periodic adjustments. Cotality notes that these modern instruments generally come with stronger consumer safeguards than many of the pre-2008 loans that helped fuel the housing bubble.

Even with those protections, the recent surge represents a notable break from long-standing American borrowing habits. The market is moving toward what Cotality describes as a hybrid era of home finance, where adjustable loans compete directly with or even displace the traditional 30-year fixed product as the leading choice in certain segments.

From Long-Term Stability to Short-Term Survival

Underlying this trend is a broader shift in homeowner priorities. With affordability as the central challenge, buyers and lenders alike are emphasizing immediate cash-flow management rather than multi-decade predictability. In that context, dynamic debt solutions — loans that can adjust or be refinanced as conditions change — are gaining institutional support.

Still, this transformation is conditional. If mortgage rates were to fall meaningfully from current levels, the calculus could flip again. A broad drop in 30-year fixed rates would likely pull many borrowers back toward the familiarity and safety of fixed payments, reducing reliance on ARM structures that expose them to future rate resets.

What to Watch Next

The current environment leaves borrowers, lenders, and policymakers watching three key variables: the path of long-term rates, price trends in high-cost markets, and regulatory oversight of adjustable products. If home values stay high and fixed rates move only modestly lower, ARMs are poised to remain a crucial gateway to ownership, especially in expensive metros and the luxury tier.

For now, the data points to a housing market where the classic 30-year fixed is no longer the automatic choice, and where short-term flexibility is often winning out over long-term certainty.